Our approach to the environment

Rising average temperatures and sea levels have been observed worldwide, making environmental challenges a truly global concern. The impact of environmental initiatives on corporate activities is expanding, driven by factors such as the Japanese government’s declaration of carbon neutrality by 2050 and the growing environmental awareness of stakeholders. The loss of natural capital and biodiversity are now recognized as critical global issues. Since corporate activities both depend on and impact these resources, it is urgent for companies to take action to conserve them.

We believe that our efforts to preserve the global environment are essential to fulfill our social responsibility and to continue our corporate activities. We will promote environmentally friendly business activities by facilitating M&As in sectors that contribute to climate change, decarbonization, low-carbon initiatives, and natural capital and biodiversity. In addition, we will work to minimize our environmental footprint by reducing greenhouse gas emissions and waste as well as procuring environmentally friendly goods.

Our Sustainability Promotion Committee is taking the lead in our environmental activities, focusing on addressing climate change in line with TCFD recommendations and nature-related issues in line with TNFD recommendations.

M&A support that contributes to the environment

By facilitating M&A engaged in solar power generation, solar power sales, and used equipment sales, we contribute to the proliferation of renewable energy and the reduction of waste and greenhouse gas emissions, with the goal of achieving carbon neutrality across society.

Disclosure based on TCFD recommendations and TNFD recommendations

- Governance

- Strategy on

addressing climate change - Strategy on addressing

natural capital and biodiversity - Risk management

- Indicators and targets

- GHG emissions

- Environmental initiatives

Governance

We have established the Sustainability Promotion Committee to identify material issues related to sustainability and make company-wide efforts to address them.

In addition to addressing overall material issues relevant to the Sustainable Development Goals (SDGs), the Sustainability Promotion Committee monitors climate-related/nature-related issues by identifying risks and opportunities, conducting scenario analyses, and calculating greenhouse gas (GHG) emissions as required by the TCFD recommendations and the TNFD recommendations, and reporting to the Board of Directors.

The Board of Directors receives reports on the status of efforts to address climate change issues, natural capital, and biodiversity, and informs the Sustainability Promotion Committee on the policies that should be adopted to address them.

Strategy on addressing climate change

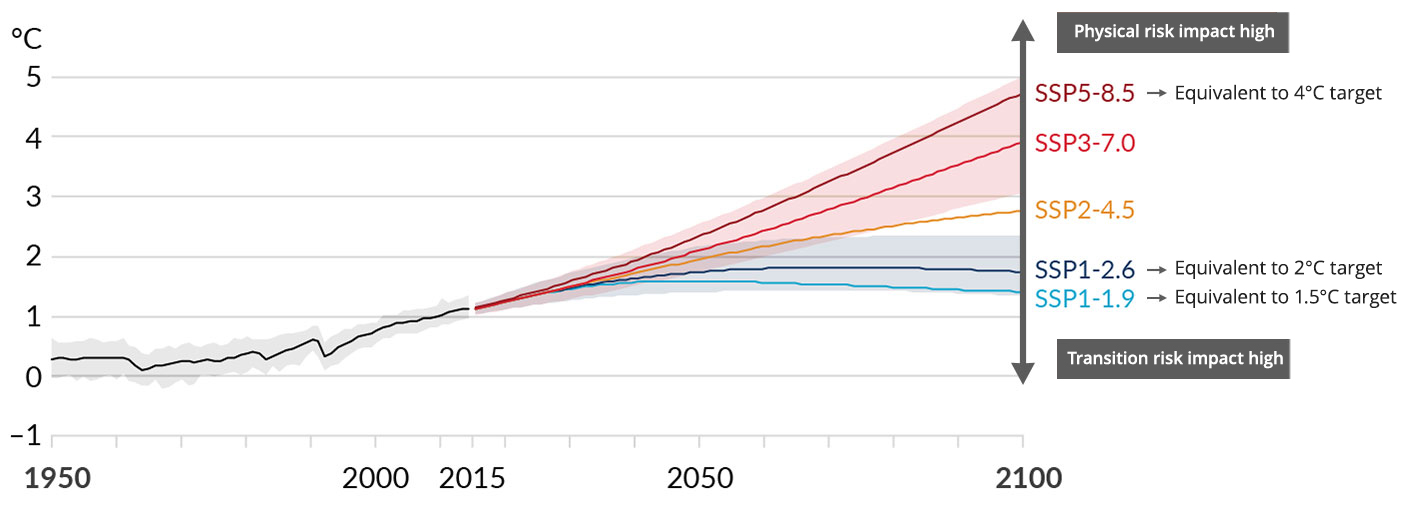

We have identified risks and opportunities that may arise as a result of climate change, in line with the TCFD recommendations, and evaluated their significance. The following scenarios were used to identify the risks and opportunities over the short, medium, and long term (2030, 2050 and 2100, respectively).

- International Energy Agency (IEA) 1.5°C rise (NZE2050), 2°C rise (APS)

- Intergovernmental Panel on Climate Change (IPCC) 1.5°C rise (SSP1), 2°C rise (SSP1, RCP2.6), 4°C rise (SSP5, RCP8.5)

Significance was evaluated by scoring the items in terms of the “degree of certainty” and the “magnitude of impact.”

- Degree of certainty: Judged based on external reports, past impacts, Our plans and policies, etc.

- Magnitude of impact:

<Risk> Judged based on severity of impact, impact on major departments, scope of impact, etc.

<Opportunity> Judged based on market size, impact on sales, competitive advantage, etc.

The most significant risks and opportunities identified through the above process are listed in the table below.

Significant risks

| Major risks | Impact on business | Significance | Time horizon | Main measures | |||

|---|---|---|---|---|---|---|---|

| 1.5°C/2°C scenario | 4°C scenario | ||||||

| Transition risk | Policy and regulatory risk | Wide-spread adoption of carbon taxes and levies as well as emissions trading schemes | Additional costs will be incurred for carbon taxes and emissions trading related to the use of fossil fuel-derived energy. | Medium | Short- to medium-term | Promote activities to reduce GHG emissions | |

| Costs will increase for emissions trading, purchase of certificates (credits), etc. to achieve the emissions targets as well as administrative procedures for reporting. | Medium | Promote activities to reduce GHG emissions | |||||

| Market risk | Increased environmental awareness of customers regarding climate change | A decrease in investment in companies with environmental risks will result in a decline in sales. | Medium | Promote environmentally friendly business activities | |||

| Physical risk | Acute risk | More frequent and severe disasters due to climate change, such as typhoons, torrential rains, and floods | Business will be suspended if the offices of our Group or those of our customers (sellers or buyers) are damaged, or if the transportation or information infrastructure connecting them is affected. | Medium to high | Medium-to long-term | Promote disaster prevention and mitigation measures at business sites, adopt remote work and use shared offices | |

| Chronic risk | Sea level rise | Risk of storm surge damage to business sites will increase and additional costs will be incurred for office relocation. | Medium | Relocate business sites, promote disaster prevention and mitigation measures at business sites, adopt remote work and use shared offices | |||

Significant opportunities

| Major opportunities | Impact on business | Significance | Time horizon | Main measures | |||

|---|---|---|---|---|---|---|---|

| 1.5°C/2°C scenario | 4°C scenario | ||||||

| Opportunity | Products/ services | Increased M&A needs of companies developing low-carbon products and services in response to climate change | The increase in the number of companies engaged in the development of low-carbon products and services will boost M&A needs as more companies will start considering M&A. | Medium to high | Short- to medium-term | Identify M&A needs of companies developing low-carbon products and services | |

| Market | Increased M&A needs of companies due to climate change | As decarbonization progresses, more companies (including venture firms) will seek to expand or create businesses in sectors that contribute to decarbonization and low carbon emissions, leading to an increase in M&A needs. | High | Identify M&A needs related to decarbonization and low-carbon business | |||

| As decarbonization progresses, there would be increased need for customers to reduce CO2 emissions in their operations, resulting in a rise in M&A needs. | Medium to high | Identify M&A needs for decarbonization | |||||

| Increased customer awareness of climate change will increase demand for investments in climate change-related businesses and therefore boost M&A needs. | Medium to high | Identify M&A needs related to climate change | |||||

| Growing environmental awareness will further require companies to address ESG-related issues, and an increase in the number of companies considering business closures will lead to an increase in M&A needs. | Medium | Identify M&A needs related to climate change | |||||

| With the setting of transaction terms that consider climate change in the market, more companies will be willing to partner with companies with large capital strength, resulting in an increase in M&A needs. | Medium | Identify M&A needs related to climate change | |||||

Business impact assessment

For the significant risks that could be estimated, we estimated the additional cost of introducing a carbon tax as a transition risk, and the additional cost of addressing the inundation of a business site in the event of flooding or storm surge (office replacement cost) as a physical risk. In the estimation, we used scenarios assuming a temperature rise of 1.5°C/2.0°C and 4°C based on information from the IPCC and the IEA.

Scenario groups used

| Temperature rise zone (2100) | IEA WEO | IPCC RCP | IPCC SSP |

|---|---|---|---|

| 4°C rise | RCP8.5 | SSP5 (fossil fuel dependent) -8.5 | |

| 2°C rise | APS (achieved in all countries that have made a net zero pledge) | RCP2.6 | SSP1 (sustainability-oriented) -2.6 |

| 1.5°C rise | NZE (net zero achieved by 2050) | SSP1 (sustainability-oriented) -1.9 | |

| Events used to estimate financial impact | Introduction of carbon tax | Flood | Storm surge |

Global surface temperature changes relative to 1850-1900

Source: Intergovernmental Panel on Climate Change (IPCC) Sixth Assessment Report (AR6) Working Group I Report on Climate Change 2021

(1) Additional costs of introducing a tax system (e.g., carbon tax) <Transition risk>

Based on information from the IEA, we calculated the additional costs that would be incurred with the emissions of greenhouse gases generated from energy consumption at our business sites.

The additional costs were larger under the 1.5°C scenario, with an impact of about 6.3 million yen in 2050. However, this amount is less than 1% of our ordinary profit for the year ended September 30, 2022, indicating that the impact of climate change is small.

| Risk | Scenario | Financial impact (millions of yen) | Financial impact (as a percentage of ordinary profit (%)) |

||

|---|---|---|---|---|---|

| 2030 (Short-term) | 2050 (Medium-term) | 2030 (Short-term) | 2050 (Medium -term) |

||

| Introduction of carbon tax | 1.5°C rise | 3.5 | 6.3 | 0.084 | 0.149 |

| 2°C rise | 3.4 | 5.0 | 0.081 | 0.119 | |

- Method of calculation

Current CO2 emissions x Future carbon tax price

- Future scenarios of carbon tax prices used

We adopted the following scenarios described in World Energy Outlook 2022 provided by the IEA.- 1.5°C rise: Net Zero Emissions by 2050 Scenario (NZE2050)

- 2°C rise: Announced Pledges Scenario (APS)

(2) Additional costs of addressing the inundation of business sites in the event of a storm surge (office replacement cost) <Physical risk>

Using future projection data provided by the IPCC, we calculated the cost of renting alternative office space (additional cost) necessary to continue our operations in the event our business sites are inundated by flooding or storm surge.

As a result of reviewing the current flood and storm surge hazard maps for all our sites, we found no locations that required inundation damage estimation due solely to flooding. Therefore, the estimation was conducted only for sites at risk of inundation damage caused by storm surges.

The additional costs were larger under the 4°C scenario, with an impact of about 24 million yen in 2100. However, this amount is less than 1% of our ordinary profit for the year ended September 30, 2022, indicating that the impact of climate change is small.

| Risk | Scenario | Financial impact (millions of yen) | Financial impact (as a percentage of ordinary profit (%)) |

||||

|---|---|---|---|---|---|---|---|

| 2030 (Short-term) | 2050 (Medium-term) | 2100 (Long-term) | 2030 (Short-term) | 2050 (Medium-term) | 2100 (Long-term) |

||

| Inundation of sites caused by storm surge | 1.5°C rise | 2.617 | 2.631 | 2.838 | 0.062 | 0.062 | 0.067 |

| 2°C rise | 7.458 | 7.458 | 9.066 | 0.176 | 0.176 | 0.215 | |

| 4°C rise | 12.919 | 15.064 | 24.232 | 0.306 | 0.356 | 0.573 | |

- Calculation method

Calculation of additional costs (future - present) due to natural disasters

Office replacement costs of each site are estimated in accordance with the national calculation method based on historical flood damage, using data published by public agencies to determine the inundation depths of the sites in the event of flooding and/or storm surge.

- Future scenarios of inundation depths used

The following scenario provided by the IPCC was adopted.

Storm surge: SSP scenario in the 6th Assessment Report (AR6) (equivalent to 1.5°C, 2°C, and 4°C rises)

Strategy on addressing natural capital and biodiversity

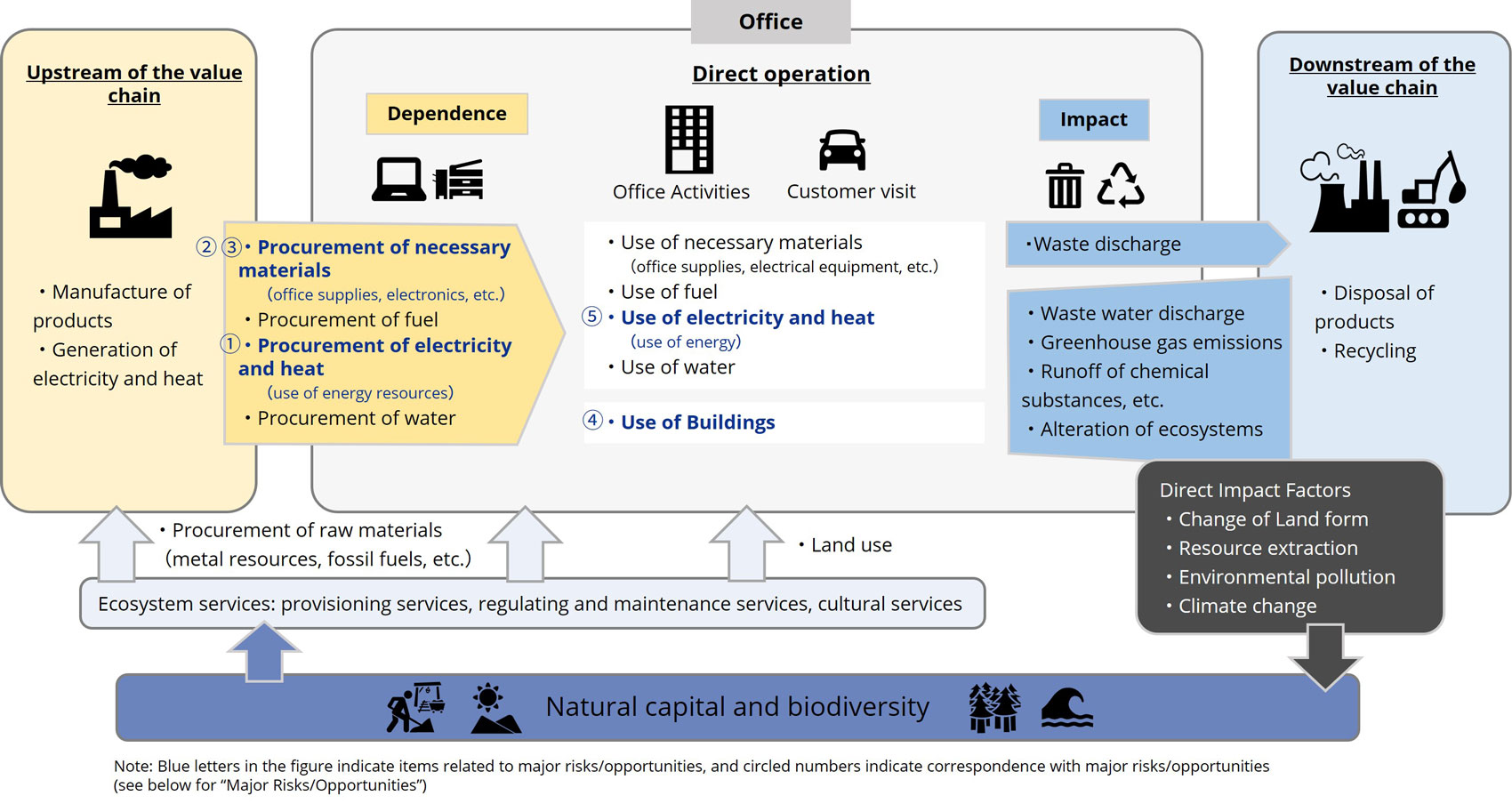

Our corporate activities depend on and influence natural capital and biodiversity throughout the entire value chain, from the procurement of necessary materials to their disposal.

Therefore, we have identified risks and opportunities that may emerge in the future based on our understanding of the relationship with nature (dependence on and impact on natural capital and biodiversity) in our business activities. In understanding the relationship with nature in our business activities, we referred to the LEAP approach* recommended by the TNFD recommendations.*LEAP approach: An integrated approach recommended by the TNFD recommendations aiming to identify and assess nature-related issues by taking four steps (Locate, Evaluate, Assess, Prepare)

*LEAP approach: An integrated approach recommended by the TNFD recommendations aiming to identify and assess nature-related issues by taking four steps (Locate, Evaluate, Assess, Prepare)

Relationship between business activities and nature

In addition to using ENCORE, a tool that provides a simplified overview of the general dependence and impact of our business activities on natural capital, we have organized our dependence on and impact on natural capital and biodiversity throughout our value chain based on the characteristics of our business.

*ENCORE (Exploring Natural Capital Opportunities, Risks and Exposure): A tool developed jointly by the Natural Capital Finance Alliance (NCFA), an international network of financial institutions, the United Nations Environment Programme World Conservation Monitoring Centre (UNEP-WCMC), and other organizations to assess the extent of private companies' impacts on and dependence on nature

We are dependent on natural capital for procurement of necessary materials such as PCs and printing paper used in our business activities, and we have an impact on natural capital through waste and greenhouse gas emissions from our business activities.

- Our ENCORE analysis was conducted on two categories of economic activities: “Financials - Investment Banking & Brokerage (Production Process: Financial Services)” and “Industrials - Research & Consulting Services (Production Process: Infrastructure Related Business)”.

- The results showed that three items (water use, water pollution, and soil pollution) had a “significant” impact in the “Industrials - Research & Consulting Services” category (no relationship in the “Financials - Investment Banking & Brokerage” category).

- Based on the actual status of our activities, the relationship with these three items is low, and therefore, we judged that the dependence/impact of our business on natural capital is low, as stated above.

Major Risks and Opportunities

The following table shows the main risks and opportunities identified as a result of our understanding of the relationship between our business activities and nature.

▶Assumed Scenarios

Based on the results of our understanding of the relationship between our business activities & nature (dependence/impact), we set up our own scenarios and analyzed risks/opportunities with reference to the natural risk scenarios provided in the TNFD guidance in order to identify nature-related risks/opportunities that may arise in the medium to long term.

▶Methodology for Materiality Assessment

The risks and opportunities analyzed were evaluated by scoring their impact on our group in terms of “degree of certainty” and “level of relevance”.

- Degree of certainty: Judged from external reports, past impacts, and our plans and policies.

- Level of relevance: Judged from the relationship between nature and our business, relevance of the contact point with nature, and the degree of impact of our business on nature, based on the idea that it is determined by the magnitude of the impact on nature x the vulnerability of nature at the site of our business activities.

| Business activities along the value chain | Relationship with nature | Risks and Opportunities | Magnitude of Importance | Examples of countermeasures | |||||

|---|---|---|---|---|---|---|---|---|---|

| Upstream | Office activity | ➀ | Procurement of electricity and heat | Dependence | Use of energy resources provided by natural capital and biodiversity supply services | Risk | Limited access to energy resources, higher fossil fuel-derived electricity prices, and higher procurement costs for electricity and heat | Medium | ・Promote activities to reduce GHG emissions |

| ➁ | Procurement of necessary materials (office supplies) | Dependence | Use of office supplies manufactured with materials provided by natural capital and biodiversity supply services | Opportunity | Procurement of environmentally friendly office supplies improves corporate image | Low to Medium | Promote the introduction of environmentally friendly office supplies ・Reduction of paper consumption |

||

| ➂ | Procurement of necessary materials (electronics) | Dependence | Use of metal resources brought about by natural capital and biodiversity provisioning services | Risk | Restricted use of metal resources, higher prices for metal products, and higher procurement costs for electronic equipment | Medium | ・Consider procurement of environmentally friendly electronic equipment | ||

| Opportunity | Procurement of environmentally friendly electronics improves corporate image | Low to Medium | ・Consider procurement of environmentally friendly electronic equipment | ||||||

| Direct | Office activity | ➃ | Use of buildings | Impact | Modification of ecosystems through the use of terrestrial ecosystems | Opportunity | Improve corporate image through greening, planting, and other activities | Medium | ・Promote solutions to local issues through social contribution activities ・Considering participation in revitalization and restoration activities(Tokyo Headquarters Office, Nagoya Office) |

| ➄ | Use of electricity and heat | Impact | Greenhouse gas emissions from energy (electricity and heat) use | Risk | Climate change-related risks will become apparent as the climate adjustment service function of natural capital and biodiversity diminishes | Medium to high | ・Promote activities to reduce GHG emissions | ||

Note: Circled numbers in the table indicate correspondence to the “Overview of Dependence on and Impacts on Natural Capital and Biodiversity throughout the Value Chain”.

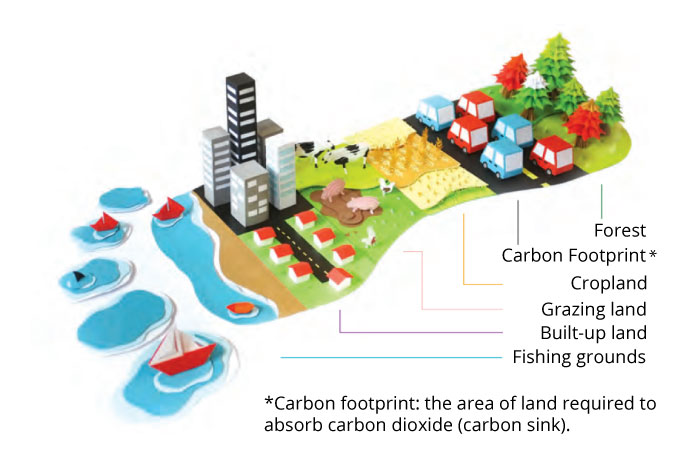

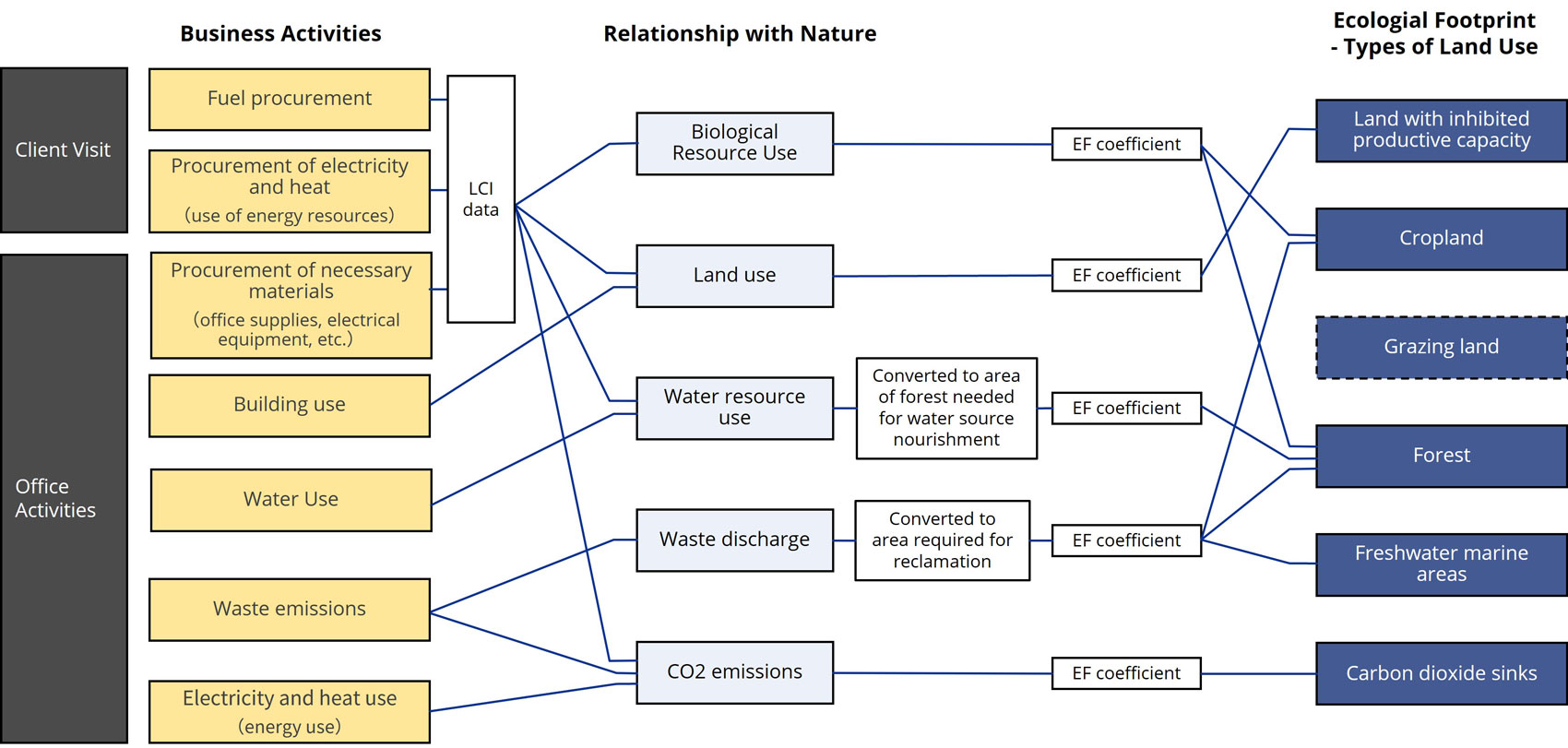

*Ecological Footprint:

Ecological Footprint adds up all the biologically productive areas to produce the natural capital needed to conduct business activities and to observe the waste that the activities consume, in terms of a hypothetical land area measured in global hectares (gha). Ecological Footprint can be used as an integrated indicator that enables integrated and quantitative assessment of multiple dependencies and impacts, even if supply chains such as procurement sources cannot be traced. The productive area is classified into six types of use: Cropland, Grazing land, Forest land, Fishing grounds, Built-up land. For non-reproducible procurement items, LCI (Lifecycle Inventory) data is used to break them down into reproducible substances that can be calculated in the ecological footprint in order to conduct assessment. (Reference: Global Footprint Network® Website)

Source: Our addition to "The Ecological Footprint for Sustainable Living in Japan (WWF Japan, 2015)

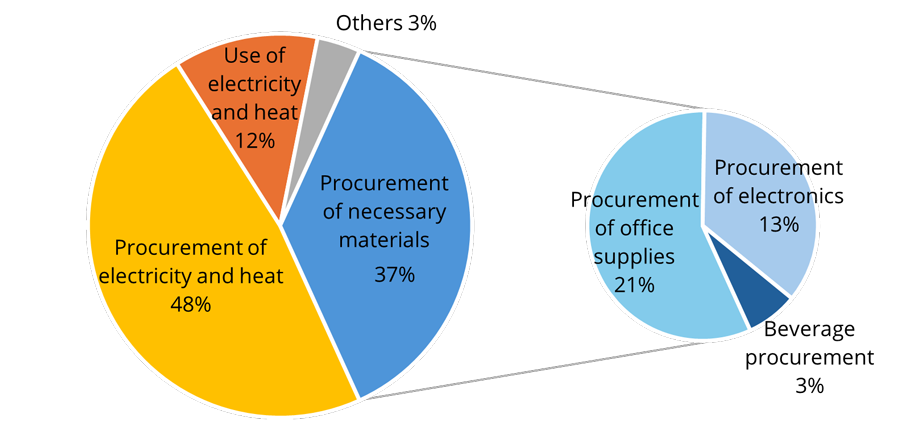

This indicates that our company has a significant dependence on and impact on natural capital for greenhouse gas emissions from our business operations and procurement of necessary materials.

Ecological Footprint Calculation Process

Percentage of Ecological Footprint

by Business Activity

Note: In case of office relocations, etc., the percentage of procurement of necessary materials will increase.

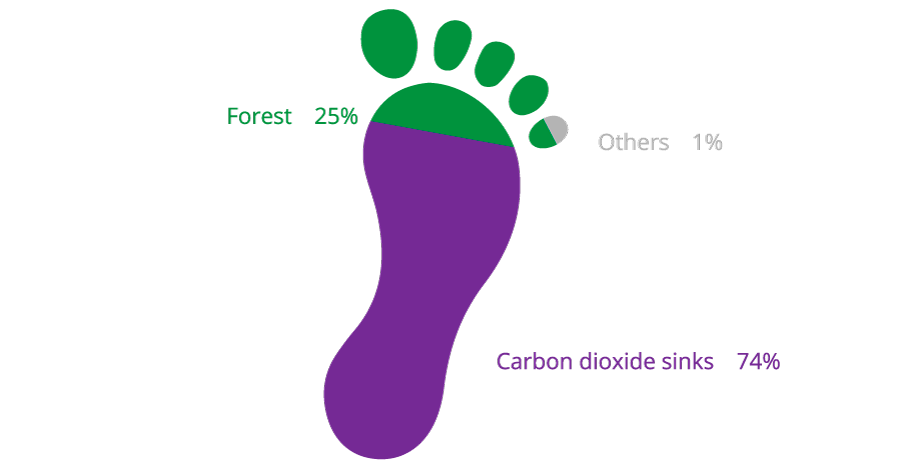

Image of Ecological Footprint

by Land Use

Analysis of Priority Locations

In the process of identifying nature-related risks and opportunities, we analyzed priority locations*.

The analysis focused on our office locations as a direct contact point with nature.

As a result of the analysis of priority locations, no sites were identified as having a negative impact on natural capital and biodiversity. However, we did identify several locations that have the opportunity to positively impact nature through revitalization and restoration activities such as greening and planting.

*Priority locations defined by TNFD:

- Material locations: locations where the organization has identified material nature-related impacts, dependencies, risks, and opportunities (direct operation and upstream/downstream value chains)

- Sensitive locations: locations where there is regarded as ecologically sensitive to assets and activities of direct business operations (direct operation; upstream/downstream value chains if possible)

| Evaluation Perspective | Analysis Indicator | Location |

|---|---|---|

| Importance of Biodiversity | Natural Park area, Key Biodiversity Area (KBA), Important Satoyama Area*, Important Bird and Biodiversity Area (IBA), Wildlife Sanctuary, etc. |

None |

| Ecosystem Health | Forest reserve, Biodiversity (Mean Species Abundance (MSA)) etc. | None |

| Water Risk | Water depletion, Cumulative withdrawals relative to demand | None |

*Important Satoyama Area: 500 sites selected by The Ministry of the Environment in Japan as rich environments that have been conserved through daily activities undertaken in local communities and conservation activities (Reference: “Satoyama in Japan” published by the Ministry of the Environment in Japan)

Example of Analysis

Source: Created by processing the latest nationwide photos (seamless) from GLOBIO web explorer (https://www.globio.info/globioweb), GSI website (https://maps.gsi.go.jp/)

Risk management

The management of company-wide risks, including those related to climate change, natural capital and biodiversity is overseen by the Director in charge of the Administration Department, and important policies are reported to the Executive Committee and the Board of Directors.

Regarding risks related to climate change, natural capital and biodiversity, the Sustainability Promotion Committee monitors the overall climate and nature-related issues by identifying climate and nature-related risks and opportunities in line with TCFD recommendations and TNFD recommendations, and reporting to the Board of Directors. Risks and opportunities identified are evaluated in terms of their significance based on the degree of their certainty and the magnitude of their impact, and those evaluated as significant are reported to the Board of Directors and incorporated into the company-wide risk management system.

Indicators and targets

We have been striving to reduce greenhouse gas emissions from our business activities in order to become carbon neutral by 2050. Based on the results of the calculation of greenhouse gas emissions for the fiscal year ended September 30, 2022, we have set the following medium-term targets.

Scope: GHG emissions (Scope 1 + Scope 2)

Target: 50% reduction by FY2030/9 compared to the base year (FY2022/9)

GHG emissions

GHG emissions results for Scope 1, 2 , and 3

Unit: t-CO2

| Classification | FY2022/9 | FY2023/9 | FY2024/9 | |

|---|---|---|---|---|

| Scope1+2+3*7 | Location-based | 2,143 | 7,346 | 5,728 |

| Market-based | 2,176 | 7,250 | 5,579 | |

| Scope 1 (fuel combustion) *1 | 18 | 22 | 28 | |

| Scope 2 (electricity use) | Location-based *2 | 95 | 131 | 290 |

| Market-based *3 | 128 | 35 | 153 | |

| Scope 2 (heat use) | Location-based *4 | 39 | 75 | 88 |

| Market-based *5 | 76 | |||

| Scope 3 (indirect emissions that that occur in the value chain of the reporting company) *6 | 1,991 | 7,117 | 5,322 | |

Subject: Strike Group Co., Ltd.

Calculation standard: Calculation based on GHG Protocol (international standard)

Scope of calculation: Scope 1 (fuel combustion), Scope 2 (electricity and heat use), Scope 3 (indirect emissions through the supply chain)

*1: Σ (Annual usage of each fuel × Calorific value per unit of each fuel × CO₂ emission factor of each fuel)

The unit calorific value of each fuel and the CO2 emission factors for each fuel are based on “System for Calculation, Reporting and Publication of Greenhouse Gas Emissions” under the “Act on Promotion of Global Warming Countermeasures.”

*2: Calculated based on the average emission factor (national average factor for FY2022).

*3: Calculated based on the adjusted emission factors by electric utility(for FY2024 submission), as specified in the “Act on Promotion of Global Warming Countermeasures.”

*4: Since the national average emission factor has not been published (as of March 2025), a substitute value (emission factor from the relevant ministerial ordinance) is used.

*5: Calculated based on emission factors by heat supplier (if the emission factors by each heat supplier is not published, a substitute value is used).

*6: The emission factors are based on values from the "Emission Factor Database for Calculating Greenhouse Gas Emissions of Organizations through the Supply Chain."

*7: Due to rounding, the sum of Scope 1, 2, and 3 may not match the total shown in the table.

Scope 3 GHG emissions results by category

Unit: t-CO2

| Category | FY2022/9 | FY2023/9 | FY2024/9 |

|---|---|---|---|

| 1. Products and services purchased | 1,106 | 3,465 | 3,099 |

| 2. Capital goods | — | 2,595 | 590 |

| 3. Fuel and energy related activities not included in Scope 1 and 2 | 33 | 61 | 106 |

| 5. Waste generated from business | 0 | 8 | 11 |

| 6. Business trip | 806 | 927 | 1,438 |

| 7. Employer commuting | 43 | 58 | 75 |

| 8. Leased assets (upstream) | 0 | 0 | 0 |

| Total | 1,991 | 7,117 | 5,322 |

* Due to rounding, the total for Scope 3 may not match the sum of the individual categories shown in the table.

Environmental initiatives

Ongoing Initiatives

The following actions are taken to address climate and nature-related risks and opportunities.

Climateindicates initiatives related to climate whereas

Natureindicates those related to nature

<Purchase of non-fossil certificates>

Climate

Nature

Since July 2022, we have been purchasing non-fossil certificates for the environmental added value of electricity derived from solar, wind, hydraulic, and other renewable energy sources, which effectively reduce CO2 emissions to zero, at our headquarters office.

<Introduction of business casual wear>

Climate

Nature

We have introduced business casual wear throughout the year and are working to save electricity by adjusting air conditioning temperatures in the summer.

<Reduction of paper consumption>

Climate

Nature

We promote the digitization and transfer of information through data to reduce waste. In addition, efforts are made to reduce paper consumption by introducing an internal decision-making system and an electronic contracting system.

<Introduction of environmentally friendly office supplies>

Climate

Nature

For office supplies, we encourage the use of products made from recycled materials, plant-derived plastics, and plastic-free alternatives.

External Evaluation

<Acquired a “B” score in CDP* Climate Change Assessment for 2024>

We have been participating in CDP's Climate Change Assessment since 2023, and this year we have received a score of “B”.

A “B” score is considered a “management level” under CDP standards and indicates that the company “understands its environmental risks and impacts and is taking action to address them”.

We will continue to actively address environmental issues and enhance transparency and information disclosure regarding the environment.

*CDP: Global NGO that operates a disclosure platform on the environmental performance of companies and government agencies